Part 2 of a multi-part research series from AQR: “Understanding Return Expectations” (downloadable at bottom of post with my highlights).

The research here focuses on the prolonged period of market outperformance of the US relative to non-US over the last 35 years, and makes the case that this is largely reflective of “richening relative valuations,” rather than solely being attributable to the underlying businesses.

Using AQR’s capital market assumptions as of December 2024, we calculate a growth edge of 2.2% p.a. for US equities to earn the same return as Non-US equities hedged to USD.

p.9

We suspect that few investors appreciate how much of the past absolute and relative performance reflects repricing, which really should not be extrapolated—especially when today’s extreme valuations point the other way.

Let’s talk about the largest problems with legacy exchange funds:

Exchange fund offerings are typically oversubscribed for tech workers. There just isn’t enough room an SP500 tracking exchange fund for large holders of $AMZN, $META, $NVDA, etc.

If you do get your shares placed, at the end of 7 years when you “could” pull out of the exchange fund, the portfolio manager will provide you with their choice of stocks (all with your initial cost basis). You no longer have a concentrated single position, but you are left with stocks that could exhibit high tracking error when compared to the benchmark.

The 351 conversion mechanism now being offered by Cache solves these issues. From my understanding, Cache can literally allow any shares into the fund. They do not have to hand-create a portfolio from subscribers. All subscribers get converted into an ETF via 351.

At the end of 7 years, you can receive shares of the ETF out of the exchange fund. Since it is an ETF, your shares will better reflect the becnhmark you diversified into.

Part 1 of a multi-part research series from AQR: “Understanding Return Expectations” (downloadable at bottom of post with my highlights).

The key concept in this paper is that individual investors tend to extrapolate heavily from recent market results, while institutional traders and capital market assumptions tend to be more “rationally anchored and contrarian.”

Investors may be losing faith in [capital market assumptions] and going all-in with the rearview-mirror mindset just when there appears to be dangerous bumps in the road ahead.

Forward-looking assessments, while imperfect, do have some positive predictive value have positive correlation of .52. Review-mirror approaches, on the other hand, are inversely correlated -.37.

The paper also discusses why individual investors might be pre-disposed to subject rearview-mirror thinking, based on Kahneman’s fast vs. slow thinking framework: “[…] past performance comes easily to mind, while required discount rates need more effortful thinking.”

The paper calls out the following 3 reasons to avoid rearview predictions in 2025:

A too-positive directional view of risky and private assets

A too-negative view on various diversifying alternatives

A too-positive relative view on US equity market exceptionalism

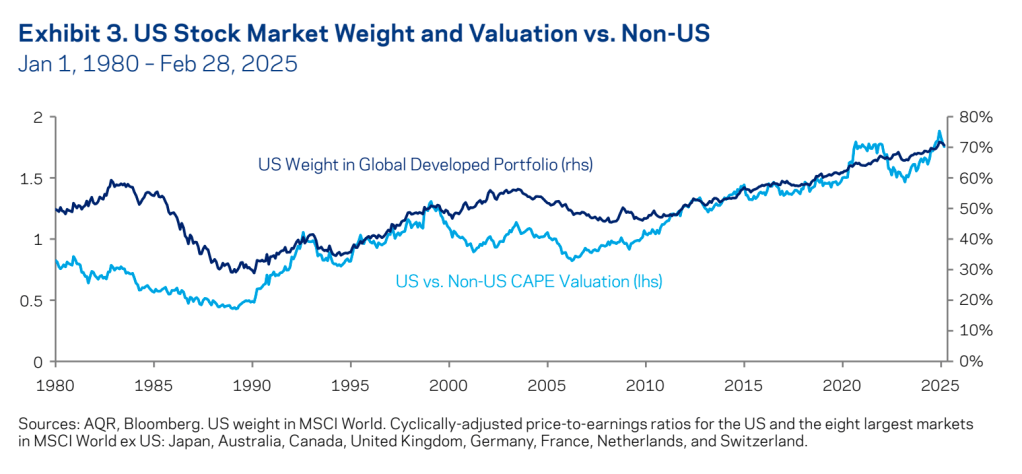

I am personally very interested that last one. Knowing that investment returns are a relative game, why would you choose to invest in a cap-weighted benchmark placing 72% of your invested assets in the US at a nearly all-time-high relative CAPE?

All these features coincide at the time of writing in the US vs rest of the world equity trade. Not surprisingly, then, US relative valuations reached almost twice the level of other developed markets near year-end 2024, having been at half-valuation level in 1990 and hovered near unity between 1995 and 2010. Despite record-high relative valuation, investors accepted a record-high 72% US weight in the MSCI developed markets index. [emphasis mine]

The real trouble with this world of ours is not that it is an unreasonable world, nor even that it is a reasonable one. The commonest kind of trouble is that it is nearly reasonable, but not quite. Life is not an illogicality; yet it is a trap for logicians. It looks just a little more mathematical and regular than it is; its exactitude is obvious, but its inexactitude is hidden; its wildness lies in wait.